The monetary independence quantity is a benchmark to find out retirement preparedness. It’s often known as the FI quantity.

The monetary independence quantity is a benchmark to find out retirement preparedness. It’s often known as the FI quantity.

Monetary independence is achieved by:

- constructing sufficient passive revenue to cowl annual bills, or

- amassing a lump sum of sufficient financial savings and investments to cowl dwelling bills via withdrawals, or

- a mix of #1 and #2.

The monetary independence quantity is the goal lump sum. Calculating the quantity solutions the query, how a lot cash do I have to cease working full-time?

Although not excellent or set in stone, there are years of information and analysis behind utilizing this single quantity to assist decide the long-term viability of a retirement nest egg.

The monetary independence quantity works nice as a baseline guidepost, however most individuals ought to tweak it to optimize long-term targets and plan conservatively in preparation for the sudden.

This text explains the origins of the monetary independence quantity, methods to calculate it, and methods to customise it on your planning functions.

Origins of the Monetary Independence Quantity

The origins of the monetary independence quantity return to the Nineties and the work of an advisor named William Bengen. Later, three professors at Trinity College revealed a paper about protected retirement withdrawal charges constructing on Bengen’s evaluation.

The three professors checked out inventory and bond knowledge from 1925 to 1975. They concluded {that a} retiree may safely withdraw 4% of their whole property per yr over any thirty years throughout that interval with out operating out of cash.

For instance, if somebody entered retirement with $1.5 million of invested property, they may withdraw $60,000 per yr for dwelling bills for the subsequent 30 years. The particular person would have a >98% likelihood of a solvent retirement.

The paper grew to become generally known as the Trinity Research, and its conclusion is the premise for the 4% rule of thumb, which we use to calculate the monetary independence quantity.

If historical past is any information for the longer term, then withdrawal charges of three% and 4% are extraordinarily unlikely to exhaust any portfolio of shares and bonds throughout any of the payout durations (from 1925 to 1995).

The 4% rule of thumb has turn out to be a vital retirement planning instrument for advisors and particular person traders.

Analysts have replicated the examine many occasions since, utilizing up to date knowledge and coming to related conclusions. An advisor and influential blogger named Michael Kitces is likely one of the extra outstanding trendy researchers.

His look on the Greater Pockets Cash Podcast is a wonderful overview of the 4% rule of thumb and different planning methods.

The right way to Calculate Your Monetary Independence Quantity

The monetary independence quantity equals annual family spending divided by 4%.

This system serves because the baseline, however most individuals ought to contemplate adjusting the quantity for his or her private state of affairs.

To calculate the quantity, first decide annual spending. Depend whole expenditures for the yr or common month-to-month bills. Remember to add estimated post-employment healthcare bills since employer advantages will stop in retirement.

I choose to make use of checking account knowledge and a spreadsheet to calculate annual bills utilizing Excel pivot tables.

After getting the annual spending quantity, divide it by 4% (0.04). Or a number of your annual spending by 25. Both manner works.

The entire is the monetary independence quantity.

We’ll use $75,000 annual spending within the examples all through this publish.

= 75,000 / .04 = $1,875,000 = 75,000 * 25 = $1,875,000

One other manner is to take your common month-to-month spending and a number of it by 300 (12*25)

= 6,250 * 300 = $1,875,000

The objective is to save lots of this whole lump sum by aggregating all investments, financial savings accounts, and different funding fairness. When you’ve hit the quantity, you’ve reached monetary independence.

Use it as a wealth-building measuring instrument to trace your invested property as a share of your monetary independence quantity (see chart on the backside).

However don’t contemplate the monetary independence quantity as an absolute finish objective as a result of there are various different elements to contemplate.

What are Invested Belongings?

Whole invested property is completely different than web value.

Some folks calculate their web value and use that to measure progress towards monetary independence. That’s simpler however much less correct.

Keep in mind, the objective is to construct a lump sum of financial savings and investments (or “invested property”) equal to the monetary independence quantity.

For a greater image, exclude the fairness worth of your major residence and different non-retirement funds resembling faculty financial savings accounts.

Do embrace the worth of fairness in funding actual property properties or different property you possibly can liquidate to purchase different income-producing property.

Moreover, suppose you generate after-tax revenue from shares, bonds, or actual property investments. In that case, chances are you’ll select to exclude the underlying property out of your invested property calculation and cut back your monetary independence quantity — extra on that under.

The right way to Customise Your Monetary Independence Quantity

One of many extra notable takeaways in regards to the 4% rule of thumb from the earlier-mentioned podcast with Michael Kitces is:

- there’s a 50% likelihood the retiree will find yourself with nearly 3X the unique financial savings

- there’s a 96% likelihood the retiree will find yourself the place they began 30 years prior

- there’s a couple of 1% likelihood of ending up with zero.

Which means the 4% rule of thumb is a conservative benchmark meant for essentially the most risk-averse.

These keen to simply accept extra threat can withdraw a bit extra, say 4.5%, and nonetheless have a very good likelihood of sustaining retirement safety for 30 years.

That mentioned, 4% could also be too dangerous for early retirees.

The 4% rule works over 30 years. For somebody of their 60s, it’s more likely to final the remainder of their lives.

However for early retirees of their 30s, 40s, or 50s, 30 years will not be a adequate planning horizon.

Thus, a extra conservative 3%-3.5% withdrawal fee could also be extra acceptable for these with an extended life expectancy or who need to go away a monetary legacy.

Decreasing the withdrawal fee is likely one of the simplest methods to cut back threat.

One other manner is to cut back annual spending.

There are different methods to customise your monetary independence quantity by accounting for extra revenue or income-producing property.

I’ve written particularly about how I measure progress towards monetary independence utilizing the F12MII quantity from my portfolio. Under is a extra common description of methods to modify the quantity.

Adjustment for Extra Earnings

Folks typically overestimate how a lot they should retire and hold working a job they don’t love.

Should you count on to obtain revenue after retirement, you possibly can cut back your monetary independence quantity and bump up your retirement date.

The obvious extra revenue stream within the U.S. is Social Safety. Youthful of us prefer to plan for retirement with out Social Safety due to doubts it should exist.

That’s an unlikely state of affairs.

Regardless of politics and deficits, all Individuals ought to count on to obtain Social Safety after they attain retirement age.

For instance, for those who count on to obtain $2,000 per 30 days in Social Safety advantages at a sure age, that’s $24,000 per yr.

Utilizing the earlier instance of $75,000 in annual bills, now you can calculate your monetary independence quantity utilizing an adjusted spending foundation. The extra revenue covers a portion of the spending.

= (75,000-24,000) = $51,000 * 25 = $1,275,000

On this instance, we’ve lowered the monetary independence quantity by $600,000, down from $1,875,000.

That shaves off a number of years of labor for those who comply with the 4% rule of thumb and don’t thoughts counting on the federal government as a part of your plan.

The lesson right here is that slightly little bit of extra revenue goes a good distance.

This sort of adjustment works effectively for Social Safety, pensions, and earned revenue (part-time work) as a result of there’s no underlying invested capital producing the revenue.

Invested capital that produces revenue is a bit completely different.

Adjustment for Earnings-Producing Belongings

Once I write about income-producing property and constructing revenue streams, I’m often referring to investments that create passive revenue. These investments embrace dividend shares, bonds, conventional and crowdfunded actual property, sure enterprise revenue, and different financial savings.

Should you regulate the monetary independence quantity down on account of income-producing property, it’s best to contemplate subtracting the underlying asset quantity from the pool of accessible protected withdrawal property.

For instance, let’s say you’ve got a $200,000 taxable dividend progress account that yields 3.0% and generates $6,000 in annual revenue earlier than tax. You possibly can cut back the premise of your yearly bills by $6,000, thus reducing your monetary independence quantity by $150,000 (= 6000 * 25).

The $200,000 shouldn’t be included in your whole invested property aggregation for those who cut back the monetary independence quantity.

Right here’s a side-by-side comparability constructing on our earlier instance. The primary is calculating the monetary independence quantity with out changes. The second adjusts for the dividend portfolio.

We’ll assume the investor has $1,000,000 of invested property.

Annual spending = $75,000 Monetary independence quantity = $1,875,000 Whole invested property = $1,000,000 Share to monetary independence = 53.33%

Annual spending = $75,000 Monetary independence quantity foundation = $1,875,000 Whole invested property = $1,000,000 Dividend portfolio worth = $200,000 Adjusted invested property = $800,000 Dividend revenue (earlier than tax) = $6,000 Adjusted annual spending = $69,000 Adjusted monetary independence quantity = $1,725,000 Share to monetary independence = 46.37%

The second instance exhibits slower progress as measured by the share of economic independence.

So why cut back the monetary independence quantity by $150,000 when you possibly can be $200,000 nearer to your preliminary goal? What’s the good thing about making this extra sophisticated?

For planning functions, you are able to do it both manner. However most of us are extra involved a couple of safe retirement than a extra imminent one.

Utilizing this technique accounts for property we don’t plan to liquidate.

Constructing and sustaining sustainable revenue streams will assist to delay retirement safety with out the only reliance on withdrawals.

Dependable revenue is important for early retirees to assist maintain prolonged retirement durations. It could possibly additionally assist fund long-term well being bills, assist relations in want, and preserve wealth to depart a monetary legacy to household or charities.

Conclusion

Years in the past, after I set a objective to retire at age 55, I anticipated that I’d be capable of generate sufficient passive revenue from dividend shares to fund my retirement life-style.

Now that I’m 49 and my retirement account balances have soared, I can retire sooner by utilizing a hybrid method to funding my retirement.

I’ll depend on each sustainable revenue from dividends and actual property, and I’ll faucet my tax-advantaged accounts after I attain age 59 1/2.

Since this realization, I’ve personalized my monetary independence quantity to account for income-producing property that I don’t intend to liquidate. The additional calculation complicates the equation a bit as an alternative of simply utilizing 25x annual spending.

Nevertheless it serves me higher, giving me an intensive image of what I want to perform to achieve F.I.B.E.R.

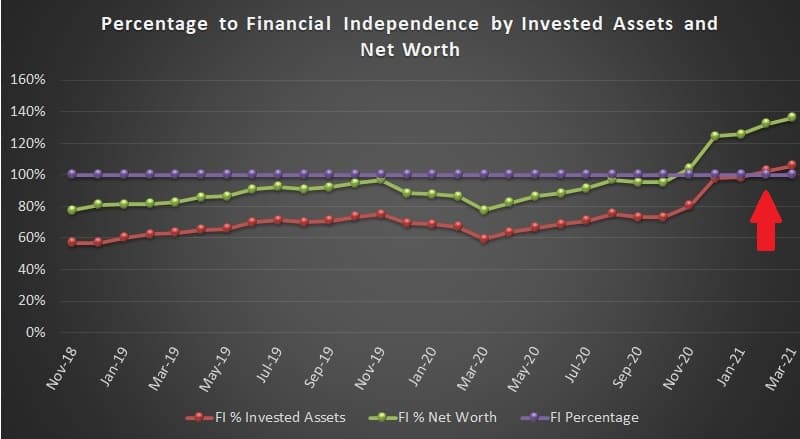

Under is a chart that I’ve been plotting since November 2018. It exhibits my web value (inexperienced) and invested property (purple) as a share of my monetary independence quantity (purple line).

I calculate my annual bills for the calendar yr. In February 2021, I reached monetary independence.

The objective is to KEEP the purple line above the purple line and develop the unfold between them till I retire.

The broader the unfold between purple and purple, the safer and comfy my retirement might be. It is going to additionally improve my probabilities of leaving a monetary legacy to my household.

Featured picture through DepositPhotos used beneath license.

Featured picture through DepositPhotos used beneath license.

Craig Stephens

Craig is a former IT skilled who left his 19-year profession to be a full-time finance author. A DIY investor since 1995, he began Retire Earlier than Dad in 2013 as a inventive outlet to share his funding portfolios. Craig studied Finance at Michigan State College and lives in Northern Virginia together with his spouse and three youngsters. Learn extra.

Favourite instruments and funding companies proper now:

Certain Dividend — Obtain the free Dividend Kings checklist, 50+ shares with 50+ consecutive years of dividend will increase. (evaluation)

Fundrise — Easy actual property and enterprise capital investing for as little as $10. (evaluation)

NewRetirement — Spreadsheets are inadequate. Get severe about planning for retirement. (evaluation)

M1 Finance — A high on-line dealer for long-term traders and dividend reinvestment. (evaluation)